Pure governance tokens seem to be just an excuse to launch a token.

I have always doubted the value of tokens dedicated purely to governance. When one thinks of a share of stock, it comes with a right to vote for corporate directors but, in practice, few people vote. Certainly, in the cases of poorly managed companies, voting comes into play when a raider acquires sufficient shares to challenge the management. But this is rare and, ultimately, the raider cares about far more than his right to vote. He cares about what control of management gets him. He cares about the assets or earnings of the company.

Similarly, when one owned a seat on an exchange, one could vote for the governance of that exchange. But, again, the real value of a seat on an exchange was the right to trade on that exchange without having to pay an intermediary.

So, why do projects issue governance tokens and do they convey any value?

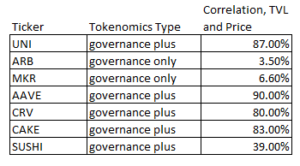

To answer this question, I examined several of the larger governance tokens. I looked at the largest tokens that CoinMarketCap categorized as governance tokens.

The problem here was that, in all but two cases, the tokens provided more than governance rights. In the case of AAVE, CRV, CAKE, and SUSHI, the token provides the right to stake and participate in the fees of the project. In the case of UNI, it was a pure governance token, but the community has recently voted to allow the charging of a protocol fee to users, that would then be distributed to owners of the UNI token.

In the case of ARB and MKR, however, these appear to be pure governance. For ARB, the gas token is ETH and ARB is only for governance. In the case of MKR, it appears to be for governance, with the risk of more MKR being minted if the project cannot pay expenses.

Measuring performance

One way to measure performance is, of course, to look at the price of the token. This, however, only tells how well the project has done. It does not tell us how well the token model has rewarded owners relative to the performance of the project.

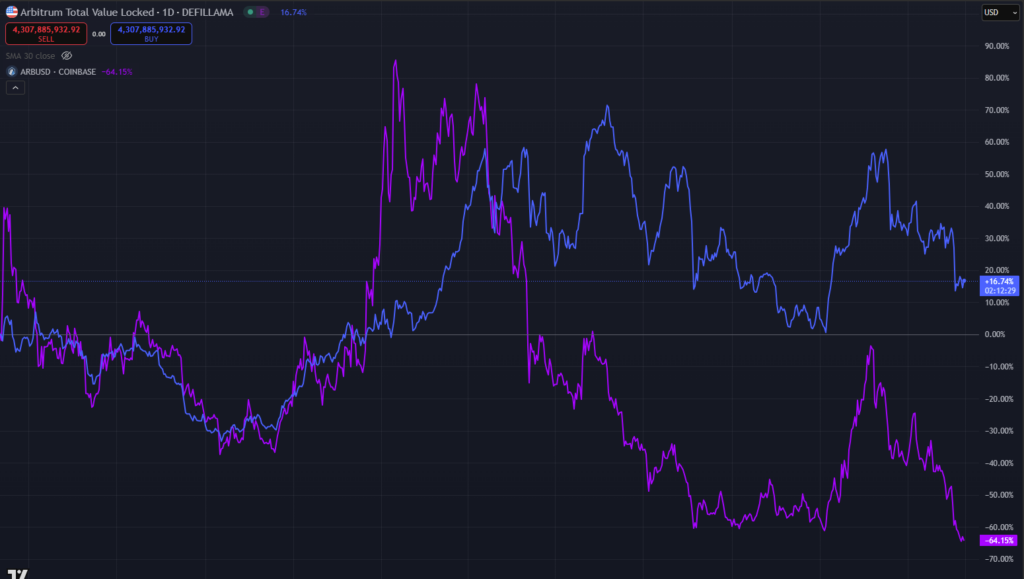

Stated differently, if ARB had drawn significant TVL over time, that would be great project performance. But if the token did not appreciate with this TVL growth, that would be bad token performance.

What I measured instead was the correlation between TVL and token price. A high correlation would mean rewarding token holders well for the success of a project, if there was success.

Results

What I found was the following:

The two pure governance tokens had very poor correlation between token price and TVL. ARB in particular has drawn significant TVL but the token has massively underperformed.

Arbitrum Token price vs Arbitrum TVL

All the projects where token owners could participate in the revenues of the project have done far better. Correlations between TVL and token price have ranged from SUSHI’s lousy 39% and AAVE’s very strong 90%.

AAVE Token Price vs AAVE TVL

Conclusions

This is an extremely small sample and more data would be very helpful. Unfortunately, there are not many token projects of a scale large enough to study.

But results are very strong and easily observed. It seems governance alone brings little to token owners. On the other hand, rewarding owners, or even the potential of rewarding owners, with some sort of revenue participation brings token performance in line with project performance.

With governance alone, a token holder can own a piece of a successful project and get no reward from it.